[ad_1]

“Regulated entities shall put in place the necessary systems and processes to implement the above guidelines at the earliest.In any case, all new retail and MSME term loans sanctioned on or after Oct 1, 2024, including fresh loans to existing customers, shall comply with the above guidelines in letter and spirit without any exception,” RBI said in a circular.

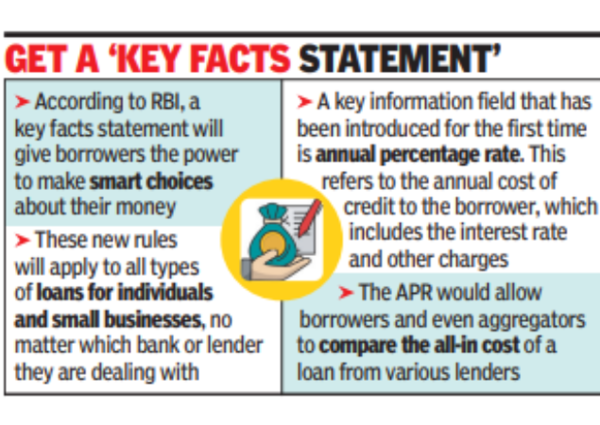

RBI said these changes would ensure that customers understand what they’re getting when they take a loan. This helps to make things fairer and gives borrowers the power to make smart choices about their money, it said. These new rules will apply to all types of loans for individuals and small businesses, no matter which bank or lender they are dealing with.

A key information field that has been introduced for the first time is annual percentage rate. This is the annual cost of credit to the borrower, which includes the interest rate and other charges. “Charges recovered from borrowers by the regulated entities on behalf of third-party service providers on actual basis, such as insurance and legal charges shall also form part of the APR and shall be disclosed separately,” RBI said.

The APR would allow borrowers and even aggregators to compare the all-in cost of a loan from various lenders.

RBI has been increasing the transparency requirement on loans since 2015. These norms were fine-tuned for microfinance institutions in 2022 and later for digital lenders in the same year. Along with the development measures announced with monetary policy in Feb this year, RBI had announced that it will introduce a requirement for key facts statement.

[ad_2]

Source link